.jpg)

Daniel Suchenski - April 26, 2016

Introduction:

While

in its purest sense globalization has been a “historical that began with the first movement of people out of Africa

into other parts of the world”[2], the history of

globalization being a household term and its general utilization as a

‘buzzword’ has perhaps only happened over the last two decades.[3] This is important to note

as the needs of the business community has changed quite dramatically in just a

few decades. While there has long been a history of international trade, and

global commerce, these issues were not nearly as common, and did not affect as

many individuals and companies as it has in the past. As the playing field has

continued to flatten and companies have needed ever-increasingly to look to new

markets for business success and world-wide profits.

Market

Entry: More finesse then prowess

The

decision by an organization to enter an overseas

market can be daunting and complex. The decision is not taken lightly and

organizational leadership and strategy play an instrumental role in the success

of such an initiative. A market entry strategy consists of both an entry mode

and a marketing plan to achieve the entry goals. Anderson and Coughlan summarize

the entry mode as a choice between company owned or controlled methods,

"integrated" channels as opposed to "independent" channels

for entry into the target country[4] The marketing mode is used

in conjunction with the marketing plan which is used to gain entry into a

target market within the target country. Albaum and Duerr define marketing plan

for market entry as: “a system composed of marketing organizations that connect

the manufacturer to the final users or consumers of the company’s product(s) in

a foreign market.”[5]

When discussing market entry options it’s important to note

that flexibility is key to success. While direct exporting may be the best

option in one country, it may be less effective or appropriate than a

joint-venture in another country and then perhaps a licensing arrangement for

manufacturing in another. Simply repeating the successes or assumptions from

one country to the next is rarely a recipe for achieving organizational goals.

Trade Start in Canada lists 9 primary options for market entry when looking to

go abroad. They are:

- Direct Exporting – “selling directly into the market you have chosen using

in the first instance you own resources.”[6]

- Licensing - “a firm transfers the rights to the use of a product or

service to another firm.”[7]

- Franchising – “the right to sell a company's goods

or services in a particular area”[8]

- Partnering – “can take a variety of forms from a simple co-marketing

arrangement to a sophisticated strategic alliance for manufacturing”

- Joint-Ventures – “a particular form of partnership that involves the

creation of a third independently managed company.”[9]

- Buying a Company – purchasing a

wholly owned subsidiary.

- Piggybacking – “If you have a particularly interesting and unique

product or service that you sell to large domestic firms that are

currently involved in foreign markets you may want to approach them to see

if your product or service can be included in their inventory for

international markets.”[10]

- Turnkey Projects – “is where the facility is built from the ground up and

turned over to the client ready to go – turn the key and the plant is

operational”[11]

- Greenfield Investments – “is where you buy the land, build the facility and

operate the business on an ongoing basis in a foreign market.”[12]

If

there is any lesson to take away from this brief overview of market entry, it

might be that even the best laid entry strategies are not fool proof and there

are any number of internal and external factors at play. Overall the entry

strategy of a company is more about brains over brawn and compromise over

arrogance. Additionally, while the marketing plan is perhaps just as important

to the success of the overall strategy, there cannot be a marketing plan for a

target country or market without first having an entry mode.

A

guest columnist for Forbes noted that there are 5 key insights that all

companies looking to enter the international market should keep in mind. 1. Educate yourself on the customs and business etiquette

of the international market. 2. Gather historical data on the country’s currency

value fluctuation and import/export timelines. 3. Become an expert on the

country’s laws governing business. 4. Conduct focus groups to test the waters

in the prospective international market. 5. Find out what your competition has

done in the same territory.[13] These 5 insights are an important backdrop for

all aspect of the strategy of entry mode and the subsequent and simultaneous

marketing plan.

While thus far the discussion

has been about consideration when your company already has both the intent and

the logistics of entering a foreign market. The question still remains, which

country should this strategy be planned for? Global Finance Magazine publishes

is rankings for the best countries to do business with and their top ten the

last 2 years have included 4 European countries, 4 East Asian countries as well

as Australia and the USA.[14] Interestingly enough all the

countries in the top 10 are developed countries. This might confuse some who

are often hearing stories of the impending takeover of the global trading

system from developing countries. One such notable group of rapidly growing

countries in the call themselves the BRICS. This acronym, which stands for

Brazil, Russia, India, China and South Africa, has grown tremendously over the

last decade and so has provided investors and companies with a great deal of

opportunity. However, despite their historic growth they may not be the clear

choice that they once were.

BRICS:

A Market Entry Example

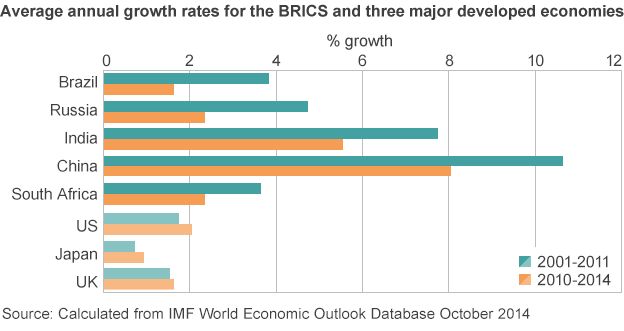

Above is a diagram

of the growth rates over the last decade of BRICS countries and leading

developed economies. In recent years there has been a slightly less bang for

your buck with regard to these countries as the recent financial troubles in

China including a significant downward expectation of its long enviable growth

rate. Both Brazil and Russia find themselves in deep recessions and recent

scandals of offshore accounts and impeachment proceedings threaten the

political stability in addition to the already present economic shakiness. S.

Africa is not much better with the chances of a recession still a real

consideration. India is perhaps the most stable relatively but even their

economy has shown signs of slowing in recent years. All these factors help

explain why Global Finance ranked Brazil (#120), Russia (#62), India (#142),

China (#90), and S. Africa (#43) all below the top 40 countries in the world

for doing business.[16]

That is not to say that these countries are not the most appropriate for a

given company to enter but that all aspects of the entry strategy need to be

brought to the table and planned for as best as possible to account for all

variables in the international marketplace including an ever-evolving business

environment that might not follow the standard by-line or buzz of a country.

Conclusion:

Using

Brazil as a more specific example for market entry, the country, like many in

the BRICS group, puts a very high importance on personal relationships. To

account for this, Export.gov and organization whose mission it is to provide

the best information and support for US companies looking to do business abroad

suggests, as part of an entry strategy that, “U.S.

firms need a local presence and thus should invest time in developing

relationships through frequent visits to Brazil.” It is also noted that any US

firm should start with the real possibility of establishing an office and/or a

joint-venture in Brazil as a way to not only understand the local needs when it

comes to marketing but also for cultural reasons that make business much harder

with someone that they have not met and does not have a ‘local’ presence.[17] Global business need to

understand the needs on the ground for not only successful entry but continued

existence after entry. These lessons will serve the marketing and export

manager well regardless of the country that the firm chooses to enter. It should

also be noted that these recent decades of ‘globalization’ are not a flash in

the pan. There is no end in sight when it comes to the interconnectedness of

the global community. Indeed, as much as the BRICS countries are expected,

despite their recent hiccups are still expected to continue growing and being

ever-more attractive places to do business. With that in mind the BRICS acronym

is unlikely the last such group that will be making headlines in years to come.

Just like when the BRICs term was coined in 2001, there are new acronyms that

are emerging that have just as much expectation and opportunity behind them as

attractive markets to grow with. Some of these include, ‘MINT’ (Mexico, Indonesia, Nigeria and Turkey), ‘CIVETS’ (Colombia, Indonesia,

Vietnam, Egypt, Turkey and South Africa), and ‘The

Next Eleven’ (Bangladesh, Egypt, Indonesia, Iran, Mexico,

Nigeria, Pakistan, Philippines, Turkey, South Korea and Vietnam).[18]

[2] “History of Globalization.” Yale

Global Online. Retrieved on 4.22.2016 from: http://yaleglobal.yale.edu/about/history.jsp

[3] C.R. “When did globalization

start?” The Economist. Published Sept 23rd, 2013. Retrieved on

4.22.2016 from: http://www.economist.com/blogs/freeexchange/2013/09/economic-history-1

[4] Anderson, E. and Coughlan, A.T. "International Market

Entry and Expansion via Independent or Integrated Channels of

Distribution". Journal of

Marketing, Vol. 51. January

1987, pp 71-82.

http://www.tandfonline.com/doi/abs/10.1080/10696679.2004.11658509

[5] Gerald Albaum and Edwin Duerr.

“International Marketing and Export Management” 7th Edition.

Prentice Hall Financial Times. 2011. Page 393.

[6] “Market Entry Strategies.” Trade

Start Canada. Retrieved on 4.22.2016 from: http://www.tradestart.ca/market-entry-strategies

[7] Ibid.

[8] Merriam-Webster Definition:

http://www.merriam-webster.com/dictionary/franchise

[9] “Market Entry Strategies.” Trade

Start Canada. Retrieved on 4.22.2016 from: http://www.tradestart.ca/market-entry-strategies

[10] Ibid.

[11] Ibid.

[12] Ibid.

[13] Lauren Maillian Bias. “A 5

Step Primer for Entering an International Market.” Forbes Published on Sep 22,

2011. Retrieved 4.22.2016 from:

http://www.forbes.com/sites/yec/2011/09/22/a-5-step-primer-for-entering-an-international-market/#14742423845f

[14] Gilly Wright. “Best Countries for

Doing Business 2015”. Global Finance Magazine. Published Nov. 12, 2015.

Retrieved on 4.22.2016 from: https://www.gfmag.com/global-data/economic-data/best-countries-doing-business?page=2

[15] Andrew Walker. “Whatever happened

to the Brics economics?” BBC World News. Published Nov. 27, 2014. Retrieved on

4.22.2016 from: http://www.bbc.com/news/business-29960335

[16] Gilly Wright. “Best Countries for

Doing Business 2015”. Global Finance Magazine. Published Nov. 12, 2015.

Retrieved on 4.22.2016 from: https://www.gfmag.com/global-data/economic-data/best-countries-doing-business?page=2

[17] “Doing Business in Brazil.” Last

updated 8.5.15. Retrieved 4.22.2016 from: http://www.export.gov/brazil/doingbusinessinbrazil/index.asp

[18] Mary Gooderham. “Beyond BRICs:

Meet the next batch of emerging markets.” HSBC Global Connections. Published

Aug. 28th 2014. Retrieved 4.22.2016 from:

https://globalconnections.hsbc.com/brazil/en/articles/beyond-brics-meet-next-batch-emerging-markets